High Net Worth Life Insurance

A high net worth client was seeking to obtain a life insurance policy of several hundred million dollars in value. This policy would help to ensure that the individual’s estate and affairs, including charitable organizations would be protected well after their passing.

Consulting Resiliency360°

As the client manages a high level of sensitive information, they wanted to ensure that their risk management strategy as well as cybersecurity framework was as resilient as possible.

Portfolio Level Political Risk Insurance

Due a global investment fund’s core objective of working with low income financial institutions, they often sought investments and capital deployments in riskier countries with often unpredictable political and market stability.

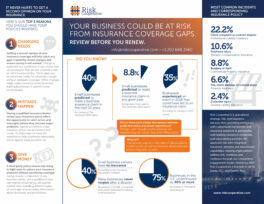

Review Before You Renew

Your business could be at risk from insurance coverage gaps. It never hurts to get a second opinion on your insurance.

Insurance 101: Business Coverage

Insurance is a necessary function for organizations, although not all view this coverage as strategically as they should. Take a closer look at what coverages are needed and when.

COVID Coverage Summary: Benefits

Many employee benefits and insurance coverage will be triggered should workers contract the COVID-19 virus. It is important to carefully review the specific language of your insurance policies to determine the extent of coverage available for the impact of coronavirus.

COVID Coverage Summary: Business Policies

As the ongoing COVID-19 pandemic continues to test organizations’ resiliency, it is important to understand how your business might be at risk. It is important to carefully review the specific language of your insurance policies to determine the extent of coverage available for the impact of coronavirus.

Property & Casualty

Risk Cooperative works with clients to provide insurance across all their property and casualty needs. Our team of risk specialists can aid with the origination, quoting and placement of property and casualty insurance solutions around the world.

Life & Health

Risk Cooperative understands that a key coverage component for any business involves life and health insurance programs. Our team has deep knowledge in these coverage areas, helping organizations to safeguard their employees anywhere in the world. Risk Cooperative provides a wide range of insurance programs for accident and health insurance, designed with each customer in mind, helping to meet their needs on a regional or global level.

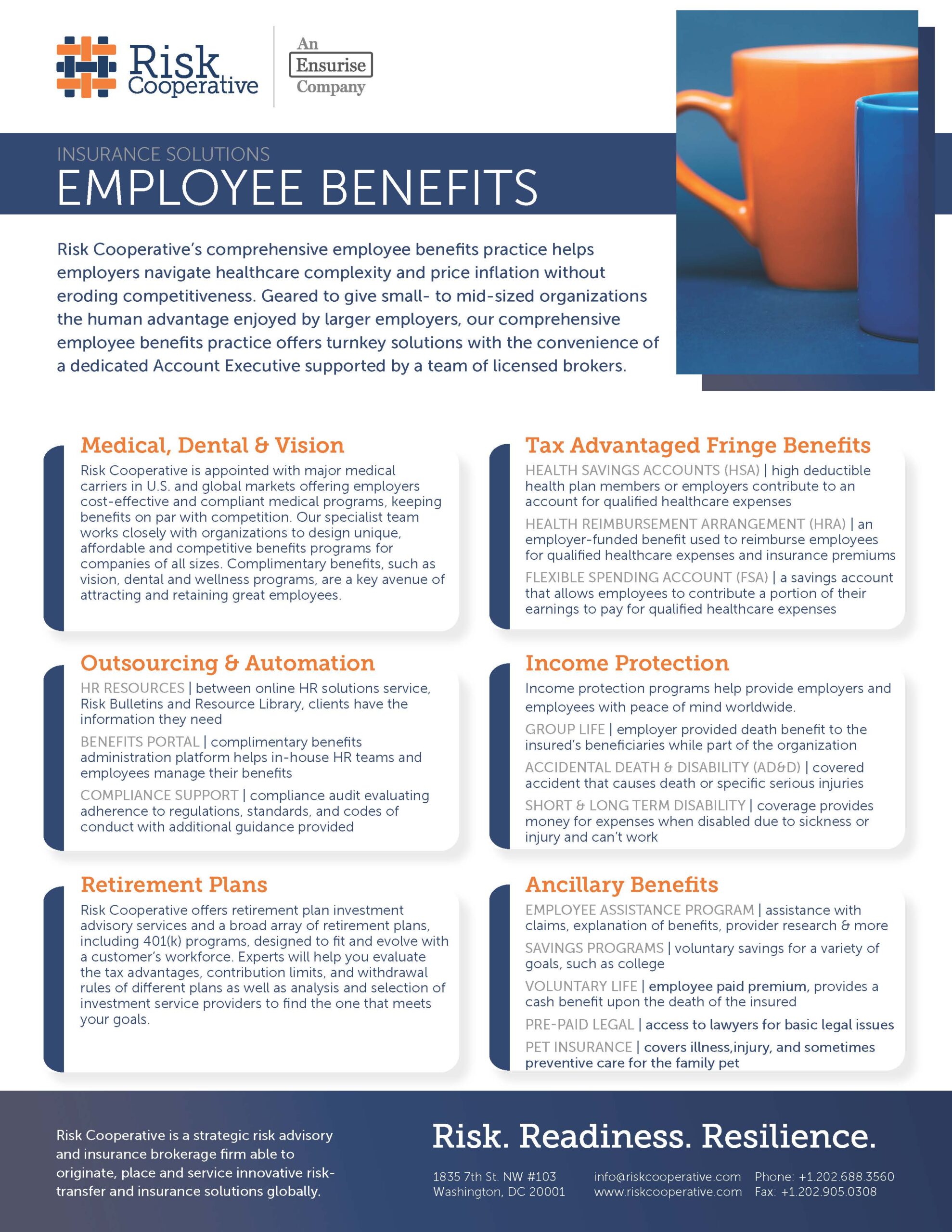

Comprehensive Benefits

Risk Cooperative’s Comprehensive Benefits practice helps employers navigate healthcare complexity and price inflation without eroding competitiveness. Geared to give small to mid-sized firms the human advantage enjoyed by larger employers, Comprehensive Benefits offer turnkey solutions with the convenience of one point of contact.

Ancillary Benefits

Ancillary benefits can be a powerful tool in an increasingly competitive talent market. Moreover, these benefits can have an outsize impact relative to their cost.

Pitfalls of Payroll Providers & Employee Benefits

Our experience working with clients requires us to advise clients to beware when utilizing payroll providers or PEOs for insurance needs. There are several pitfalls to avoid when these firms claim their buying power allows them to help control rising healthcare costs.